The CISC is the voice of the Canadian steel construction industry. We are proud to be the premier organization in creating solutions for the critical issues that challenge the steel construction industry every day.

U.S. Section 232 Tariffs Lifted Against Canada, U.S. Anti-Dumping Action Continues

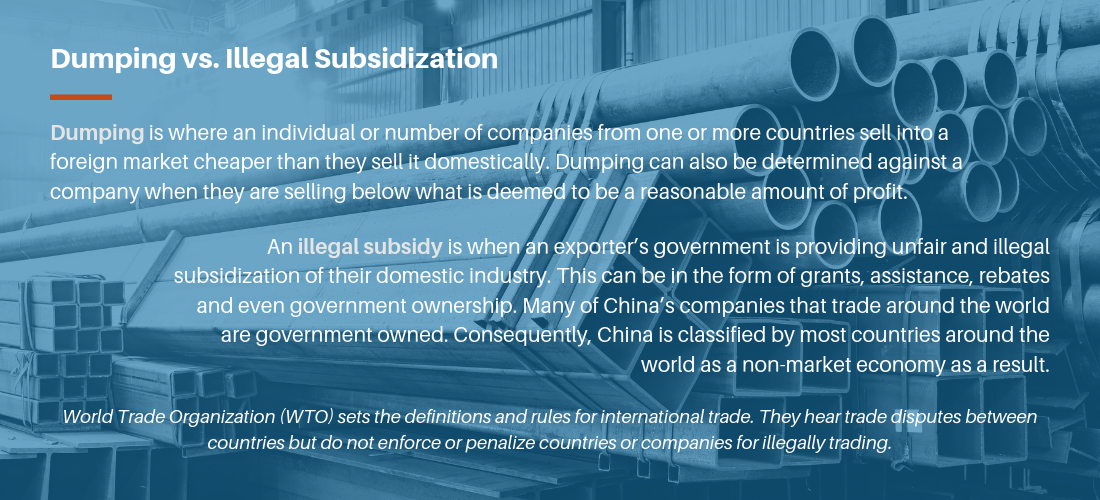

U.S. Section 232 tariffs against Canada and Mexico were eliminated on May 20, 2019. The resolution was primarily fueled by the U.S.’s wish for the quick passage of the United States-Mexico-Canada Agreement (USMCA) by all three countries. The Section 232 resolution only applies to the shipment of raw steel and aluminum across the Canadian, U.S. and Mexican borders and does not apply to any other trade dispute at present. The American Institute of Steel Construction’s (AISC) anti-dumping and countervailing duties (illegal government subsidies) against Canada is not affected by this resolution.

The impacts were as follows:

- Elimination of the Canadian retaliatory tariffs to Section 232.

- Termination of Section 232 WTO litigation by Canada against the U.S.

- Implemention of measures by both countries to prevent dumped and subsidized steel and aluminum flowing across the border to either country.

- Implementation of measures to prevent dumped and subsidized steel and aluminum prices in each country.

- Implementation of a mechanism that triggers mutual discussion resulting on surges that affect each other’s market share in each other’s country. A country may impose a 25 per cent steel tariff on the surged product against that country.

AISC’s Anti-Dumping and Countervailing Duty Case Against Canada Update

On February 4, 2019, the AISC launched a petition for the imposition of anti-dumping (AD) and countervailing duties (CVD) against Canada, China and Mexico on fabricated structural steel. The AISC has made claims that Canada is illegally pricing fabricated steel, in addition to receiving illegal subsidies from Canadian governments.

On February 25, 2019, the U.S. International Trade Tribunal filed a ruling that allowed the case to proceed with the investigations and timelines prescribed.

At present the two trade cases (AD & CVD) are still ongoing and are being investigated by the U.S. Department of Commerce (DOC), with the following upcoming dates to keep in mind:

- July 5, 2019 (extended date) – Preliminary CVD Determination

- July 15, 2019 – Preliminary AD Determination

- *September 3rd (if extended – very high chance) – Preliminary AD Determination

It is important to note that these are two different and separate investigations. The CVD case is about illegal government subsidization and will be the first to report out. Even though the top two exporters happen to be from Quebec, the DOC is investigating all government programs across Canada with the exception of Newfoundland. Any assessment of countervailing duties will be from a combined assessment of Federal and all provincial programs.

If the DOC determines that there is no illegal subsidization and not over the minimum threshold of 1% the CVD case ends on July 5th. There may be several days delay before the announcement is made public and provisional dues applied. Similarly, the same holds true for the AD case.

In the case for AD determination, the provisional Canadian duty assessed and levied (if determined) will be the average of duties assessed for each of the 2 companies being investigated.

Prompt Payment Legislation Spreads Across Canada

To date the following provinces have passed prompt payment legislation and have included adjudication as part of their framework:

- Ontario

- Nova Scotia

- Saskatchewan

Although legislation has passed in all three provinces, it will be some time for each government to write the regulations and to begin implementation. Ontario is expected to be the first of the three provinces to enforce prompt payment legislation as early as this fall.

Quebec is doing things slightly different by running a pilot project with draft prompt payment regulations. Adjudication is not included. The program is expected to be in full effect for all construction projects within several years.

Manitoba’s first legislative try was not successful but another improved prompt payment piece of legislation is in front of the legislature with hopes it will pass very soon.

BC had prompt payment legislation introduced by the Liberal opposition. Although we are happy BC is now moving forward with legislation, this legislation does not include adjudication which CISC believes is the most important mechanism to ensure speedy and unbiased resolution to disputes. The CISC will engage the members on all sides to get adjudication included in the amendments.

The federal prompt payment legislation has been reviewed by both the House and Senate working committees. Representatives of the National Trade Contractors Coalition of NTCCC (which the CISC is a member) have spoken for our support of the bill. It is expected to pass before the end of June.

Fabricated Industrial Steel Components (FISC) Trade Case Update

In 2017, the CISC and our industrial steel fabrication partners won a world precedent case on fabricated steel. The Canadian International Trade Tribunal (CITT) levied anti-dumping duties of 48 per cent on China, South Korea and Spain. China was also found to be illegally subsidizing their steel fabrication industry by 50-70 per cent. This ruling granted Canada five years of protection from these countries with the possibility of renewal for another five years.

Shortly after our win, Fluor, Suncor and others appealed the CISC’s FISC case arguing that modular construction does not include fabricated steel but rather a manufactured product, and therefore duties should not apply. The appeal was heard in April 2018 at the Federal Court of Appeal. The final ruling from the court has yet to be released.

The CISC has defended two scope ruling cases in 2018. Importers or exporters have the right to argue their products do not fall within the scope of the FISC case. In both cases, the CISC was successful in arguing that the products are indeed FISC and fall within the scope of the ruling. More scope ruling requests are expected in 2019.